product

Your Customers Don't Know What a Deductible Is. Your Interface Is Making It Worse

The premise nobody wants to say out loud

The premise underneath most digital insurance enrollment flows is that the customer understands the product. They know what a deductible is. They know what a coinsurance rate means. They can mentally compare two plans on out-of-pocket maximums while holding network restrictions and premium differentials in working memory. The interface, in this view, just needs to be efficient: present the options cleanly, let the customer choose.

The evidence on what insured consumers actually understand suggests this premise is wrong, and not by a small margin.

What the data show

Three pieces of evidence anchor this discussion.

Loewenstein et al. (2013), in the Journal of Health Economics, surveyed two representative samples of insured Americans on fundamental insurance concepts: deductibles, copayments, coinsurance, out-of-pocket maximums, in-network versus out-of-network distinctions. The majority of respondents did not correctly understand these basics. The pattern was not driven by recent enrollment; it persisted across tenure of coverage.

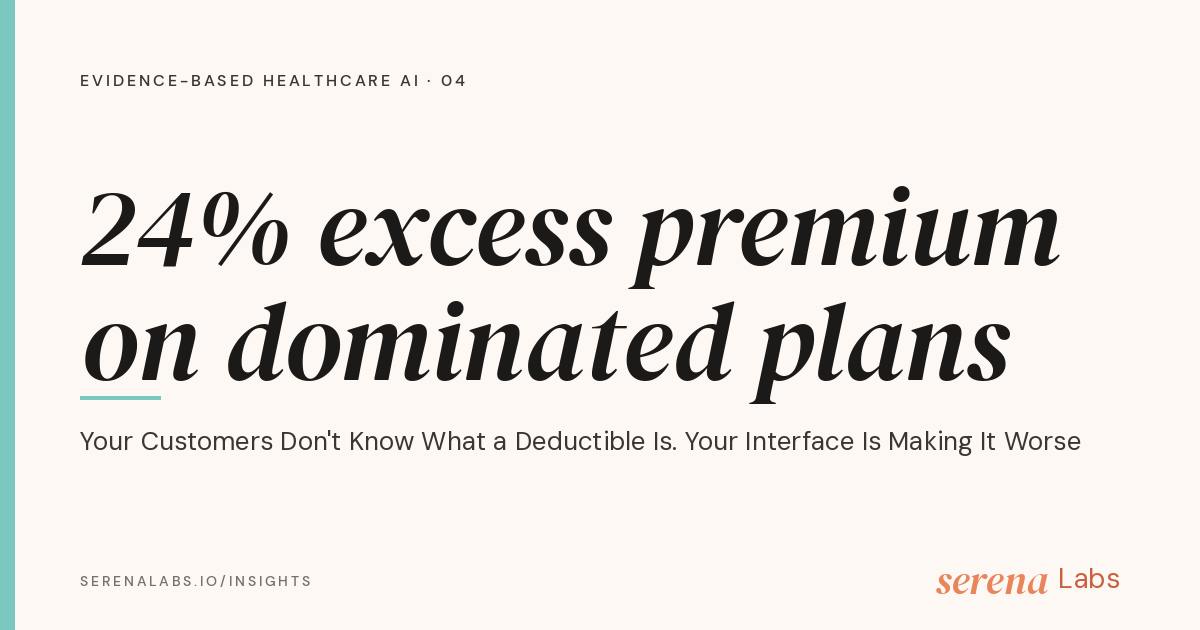

Bhargava, Loewenstein, and Sydnor (2017), in the Quarterly Journal of Economics, analyzed plan selections by N = 23,894 employees of a large U.S. firm choosing from a structured benefits menu. The result that put the study on the syllabus of every behavioral economics course: the majority chose financially dominated plans. A "dominated" plan is one that costs the consumer strictly more in every realized health-spending scenario than an alternative on the same menu. There is no rational case for choosing it. The majority did.

The excess spending was substantial: approximately 24% of chosen premium. Translating that to dollars: tens of millions of dollars annually for a single firm's workforce, allocated to plans that were measurably worse on every dimension than the alternative one click away. The pattern persisted even among highly educated respondents, which rules out the comforting interpretation that this is just a "low-education population" problem.

Williams et al. (2023), in Cancer Medicine, conducted a mixed-methods study of cancer survivors making health insurance decisions (N = 80 quantitative, N = 20 in-depth follow-up interviews). Using the validated HIL Measure instrument, median scores fell in the low-to-moderate range. The qualitative data was the most striking part: low-HIL respondents reported attending more to the most confusing benefit categories (deductibles, hospitalization costs), but still failing to integrate that attention into a coherent decision. More cognitive effort, same poor outcomes.

The combined picture: the population of insurance customers is, in aggregate, systematically under-equipped to formulate the questions that an open-ended interface would ask them to formulate, and to integrate the answers that a self-service interface would expect them to integrate.

What Health Insurance Literacy actually is

A recent critical interpretive synthesis by Ron et al. (2025a) in Health Policy consolidates two decades of HIL research. The framework integrates HIL across three competencies:

Comprehension: understanding insurance terms, structures, and trade-offs

Confidence: self-efficacy in making and acting on insurance decisions

Navigation: practical ability to operate the systems and interfaces through which insurance is selected and used

The accompanying validation study (Ron et al. 2025b in BMC Health Services Research) confirmed that these are psychometrically distinct dimensions: a person can score well on one and poorly on another. The implication for interface design is direct. A customer with adequate comprehension but poor navigation cannot use a self-service enrollment flow effectively, even if they could pass a quiz on deductibles. A customer with adequate navigation but poor comprehension can complete the flow and pick the wrong plan.

If your interface treats HIL as a single dimension (or treats it as not relevant at all), it will systematically fail on the populations where any one of these competencies is the binding constraint. In the general population, that is most of your customers.

How most enrollment interfaces respond to this

Most don't. The default response is one of three patterns:

Pattern 1: Pretend it's not a problem. Build the interface as if the customer is an informed shopper. Provide a search field, a sort function, a comparison table. Treat insurance plans as if they were retail products. This pattern is most common in private exchange platforms and was the original ACA Marketplace design. Johnson et al. (2013), in a PLOS ONE experiment approximating the ACA user base across six studies, documented that unaided choice in this format produced consumer-error costs of approximately $533 per person versus a baseline of optimal selection. Scaled to the marketplace population, the authors estimated a cost to consumers of roughly $9.12 billion per year.

Pattern 2: Stack disclosures. Comply with regulatory disclosure requirements (the Summary of Benefits and Coverage in the U.S., the suitability assessment under IDD in Europe, the disclosure norms under ANS in Brazil) by placing them prominently and assuming the customer reads and integrates them. This pattern is most common in IDD-compliant European platforms. The evidence on whether stacked disclosures change actual decision quality is, at best, mixed.

Pattern 3: Add a chatbot to "help". Layer an open-ended conversational interface on top of the existing flow. The intuition is that the chatbot will answer questions and explain concepts. The evidence, covered in our companion piece on the preference–performance paradox, suggests that open-ended chatbots worsen the underlying problem: they presuppose that the customer can formulate domain-appropriate questions, which low-HIL users by definition cannot. The chatbot ends up answering the questions the customer knows to ask, not the questions the customer would have needed to ask.

All three patterns share a common failure mode: they treat HIL as the customer's problem to solve, not as a structural constraint the interface must absorb.

What works

The interface design pattern that the evidence supports is closer to literacy-adaptive scaffolding than to either self-service or open-ended dialogue.

The components, in design-requirement terms:

Detect or infer HIL level. Through interaction signals (response time, vocabulary, sequence patterns) or through a brief upfront screener. Adapt the scaffolding intensity accordingly. High-HIL users get streamlined flows; low-HIL users get more decomposition, more inline explanation, more guided comparison.

Sequential decomposition respecting working-memory limits. Multi-attribute insurance decisions exceed unaided cognitive capacity for any user, but the absolute capacity gap is largest for low-HIL users. Sequential steps with summary checkpoints reduce extrinsic cognitive load. Cowan's estimate of approximately four elements of active working memory is a more conservative benchmark than Miller's classical 7±2 for high-stakes decisions, and is more appropriate for HIL-vulnerable populations.

Choice architecture by design. Dellaert et al. (2024), in the Journal of Marketing, conducted a randomized experiment combining one field study and three lab experiments (N = 3,866 across treatment conditions). Combining ordering (ranking plans by estimated profile fit) with partitioning (structuring the choice set into salient subgroups) produced economically significant consumer welfare improvements, robust across demographic subgroups when the ordering quality threshold was met. This is not a soft "nudge"; it is a measurable improvement in decision quality on real benefits choices.

Inline education at decision points, not as a separate help section. Low-HIL users do not navigate to "Learn more" pages. Definition and trade-off explanation must arrive in the same screen as the choice, at the moment it is needed, in language calibrated to the inferred HIL level.

Equity-disaggregated outcome reporting. Measure your enrollment flow's performance separately for the bottom HIL quartile. Average outcomes will obscure the most important signal. The operators who care about consumer welfare (and, increasingly, the regulators who oversee them) will look at distributional outcomes, not averages.

The qualitative evidence from real ACA enrollment captures the consequence of getting this wrong. Faugno et al. (2023), in Health Policy OPEN, documented through qualitative interviews how consumers describe the non-group plan selection experience: as akin to "rolling the dice." That is the experience a low-HIL customer has on a high-friction enrollment interface. It should not be the modal experience for a regulated consumer-finance product.

What this implies for product strategy

Three operational implications.

First, the addressable cost of poor HIL design is large and quantifiable. Johnson et al.'s $9.12 billion annual marketplace-level estimate is not a hypothetical. Bhargava's 24% premium-equivalent excess spending is not a hypothetical. The number you should compute for your platform is what fraction of your customers are choosing plans they would not have chosen with adequate decision support, measured by plan–profile adequacy scoring. That number is your HIL-design liability.

Second, the equity dimension is not a nice-to-have. When your interface performs adequately for high-HIL customers but poorly for low-HIL customers, the welfare loss falls on the population least equipped to bear it. For mission-driven payers, public exchanges, and IDD/ANS-regulated entities, this is a regulatory and brand exposure, not just a UX detail.

Third, "add an AI to it" is not a solution. It can be part of a solution, in the right places, with the right structure. Generic AI assistance on top of a self-service flow that already assumes literacy will not solve the underlying problem and may make it worse.

What Serena Labs does

Serena Labs builds AI-driven engagement for healthcare with literacy-adaptive scaffolding at the core of the configuration and selection layer. We use interaction signals to infer HIL level, adapt scaffolding intensity in real time, and apply choice architecture (ordering, partitioning, intelligent defaults) by construction. We benchmark performance by HIL segment, not just on aggregate completion, because the equity outcome is what determines whether the platform is doing its job.

If you operate enrollment for an insurer, a marketplace, or a regulated benefits program and the HIL distribution of your customer base is on your radar, talk to our team.

Read next

This piece is part of a series on evidence-based healthcare customer engagement. The pillar overview, "Beyond AI Chatbot Hype: An Evidence-Based Framework for Healthcare Customer Engagement", lays out the full contingency framework. See also the companion piece on the preference–performance paradox.

Key references:

Bhargava, S., Loewenstein, G., & Sydnor, J. (2017). Choose to lose: Health plan choices from a menu with dominated options. The Quarterly Journal of Economics, 132(3), 1319–1372. doi.org/10.1093/qje/qjx011

Dellaert, B. G. C., Johnson, E. J., Duncan, S., & Baker, T. (2024). Choice architecture for healthier insurance decisions: Ordering and partitioning together can improve consumer choice. Journal of Marketing, 88(1), 15–30. doi.org/10.1177/00222429221119086

Faugno, E., Gilkey, M. B., Cripps, L. A., Sinaiko, A., Peltz, A., Kingsdale, J., & Galbraith, A. A. (2023). "Pick a plan and roll the dice": A qualitative study of consumer experiences selecting a health plan in the non-group market. Health Policy OPEN, 5, 100112. doi.org/10.1016/j.hpopen.2023.100112

Johnson, E. J., Hassin, R., Baker, T., Bajger, A. T., & Treuer, G. (2013). Can consumers make affordable care affordable? The value of choice architecture. PLOS ONE, 8(12), e81521. doi.org/10.1371/journal.pone.0081521

Loewenstein, G., Friedman, J. Y., McGill, B. A., et al. (2013). Consumers' misunderstanding of health insurance. Journal of Health Economics, 32(5), 850–862. doi.org/10.1016/j.jhealeco.2013.04.004

Ron, R., Feder-Bubis, P., Trocha, K., & Ellen, M. (2025a). A new integrated conceptual framework of health insurance literacy: Results of a critical interpretive synthesis. Health Policy, 161, 105394. doi.org/10.1016/j.healthpol.2025.105394

Ron, R., Ellen, M. E., & Feder-Bubis, P. (2025b). Development and validation of a new comprehensive measurement tool for health insurance literacy. BMC Health Services Research. doi.org/10.1186/s12913-025-12881-9

Williams, C. P., Platter, H. N., Davidoff, A. J., Vanderpool, R. C., Pisu, M., & de Moor, J. S. (2023). "It's just not easy to understand": A mixed methods study of health insurance literacy and insurance plan decision-making in cancer survivors. Cancer Medicine. doi.org/10.1002/cam4.6133